Since the 2009 recession, our economy has expanded at double the rate of other American metropolitan areas. [2] Since 2010, the region has added around 600,000 jobs, bringing the Bay Area’s total employment to a historic high of 4.1 million jobs.

What’s happening in the Bay Area economy is a classic example of an economic cluster. When groups of firms in similar and related industries group together, along with many people possessing the skills those firms need as well as supportive institutions (like investors who understand that industry), a form of economic growth can happen that becomes self reinforcing.

Firms that want to succeed in that industry (and the employees who work within it) have better chances if they locate in the same place. The key elements of the Bay Area’s innovative cluster include a highly educated and mobile workforce, the region’s large share of venture investment (fully half of all venture investment in the country [3]), and a unique culture of openness and experimentation.

But successful clusters never last forever. Just ask Detroit, one of the most successful and innovative clusters in the world for more than half a century.

It’s sometimes hard to perceive the long-term trajectory of economic clusters because of how dramatic the more short-term, cyclical ups and downs of the business cycle are. We know that booms and busts are an inevitable part of capitalism, but what do we know about the longer-term fate of the Bay Area innovative economy?

What we know is that the talent needed to start companies — especially knowledgeable investors, entrepreneurs, and engineers — appears to be increasingly concentrated here. Yet our economy is outgrowing our physical place. Neither regional transportation infrastructure nor the housing supply is keeping pace with the job growth. The transportation and housing constraints are the result of deep-seated, long-standing policy problems (and the subject of much of SPUR’s work).

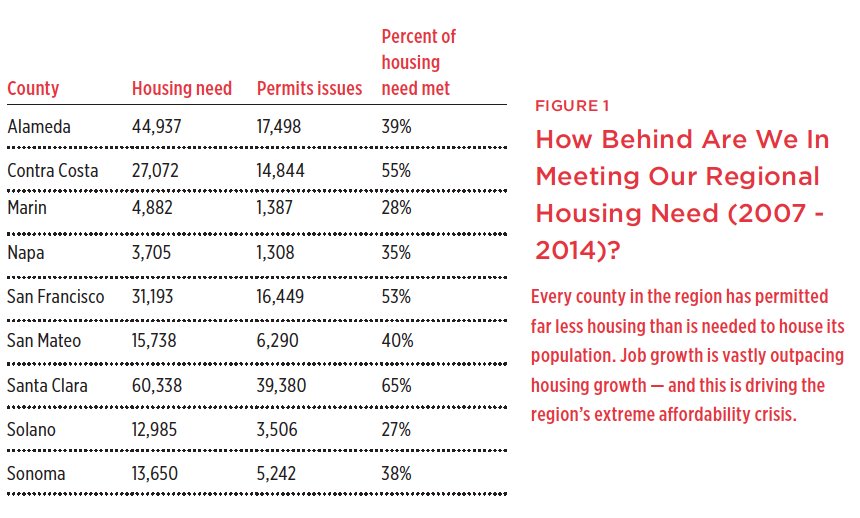

Job growth is vastly outpacing housing growth, and this is driving the region’s extreme affordability crisis. While the Bay Area has added roughly 600,000 jobs over the last five years, we have built just 55,000 new units of housing. As the pace of adding jobs has accelerated, the pace of adding housing has slowed over the past two decades. The severity of the imbalance of jobs and housing varies throughout the region. The good news includes the fact that an increased proportion of housing has been built as multifamily units and in urban areas near transit, and this kind of density contributes positively to the region’s goals for accommodating growth sustainably. But we need far more of it. Every county in the region has built significantly less housing than regional projections say we must in order to accommodate increasing population numbers.

Something quite similar is happening in transportation. Though the region has added 600,000 new jobs in the last five years, it has not made the corresponding investments in transportation infrastructure necessary to move people to and from these jobs.

The consequence is dismally familiar to anyone commuting in the region today: Caltrain and BART are at capacity and the freeways and bridges are parking lots. Commutes that used to take 40 minutes now regularly take over two hours. It is going to take a generational reinvestment in transit infrastructure to remedy the deep hole we’ve gotten into. While we talk about high-speed rail into downtown San Francisco, a second Transbay tube, BART to Silicon Valley, and major investments the Capitol Corridor, do we have it in us to fund and build them?

It is inevitable that we will be in competition with other regions; tech jobs are already spreading to many other places. But it is our own actions – or rather, nonactions – that seem most likely to be the existential economic threat in the long run. It is possible that these choices and contradictions may lead to long-term decline of the Bay Area economy.

Another possibility is that we become a region dominated by very high-end, expensive businesses exclusively – generally what we refer to by the category of “tech” today. Given its ability to pay top dollar for space and talent in an up-cycle, tech will be able to best weather the downsides of being here and out-compete other industries that can’t. It is the diversity of our economy — and the diversity of the people who hope to find a place in that economy — that will suffer. We are already seeing this.

There is a third possibility: The region could solve the problems it faces. We could make massive new investments in our transit system and we could dramatically change course on housing policy by allowing the supply to grow in many more cities around the region.

We know that there will be another recession; this seems an inherent part of the capitalist economy. What we don’t know is the long-term prospects for our region, and that depends on the choices we make.

Endnotes

[1] Based on Plan Bay Area projections for 2030 (4.19 million) compared with Association of Bay Area Government’s estimate of 2015 year-end total actuals (4 – 4.1 million).

[2] Other metro areas studied included New York, Los Angeles, Austin, Boston, Seattle and San Diego. As cited in “A Roadmap for Economic Resilience” (The Bay Area Regional Economic Strategy, Bay Area Council Economic Institute, San Francisco, CA, 2015).

[3] “A Roadmap for Economic Resilience” (The Bay Area Regional Economic Strategy, Bay Area Council Economic Institute, San Francisco, CA, 2015).