(This article is based on a longer report produced by ICF International and Business Cluster Development.)

In a time when climate change is becoming unavoidably tangible for more and more of the world’s population, when consumers increasingly demand to know what environmental impacts their lifestyle choices will bring, and prices for fossil fuels seem destined for the stratosphere, many people find themselves thinking, “There’s got to be a better way.”

There is indeed a better way — or, rather, a great many potentially better ways — and the Bay Area and San Francisco are a hotbed of the kind of innovations that are making it possible to do business in cleaner, greener ways than ever before. Every day in the Bay Area, companies are conducting research and development (and investors are providing the venture capital dollars that make it possible) on groundbreaking technologies that are enabling businesses to provide new products and services, or to keep doing the things they’ve been doing for years, but with less energy or a reduced impact on the environment. Collectively, these innovations in cleaner technologies are known as “cleantech.”

The search for cleaner technologies originated with state and national environmental regulations in the 1960s and 1970s, as companies sought to comply with rules governing the production of industrial waste. But now, many more companies are looking for greener ways of doing things not just because consumers insist upon it, but also because advancements in technologies mean that cleantech solutions are becoming more cost competitive and implementing them can reduce the cost of doing business or help companies fill consumers’ demands. Cleantech now makes good business sense.

While many have written about the coming green economy, too little of the focus has been about pinning down the exact position of cleantech in the local economy. SPUR commissioned a study to determine just how many local cleantech businesses exist in the Bay Area today, where they are located, what types of cleantech work they’re doing, how they fit into the economy and what conditions are essential to their success.

Why is cleantech important for the local economy?

By developing its cleantech industries, San Francisco can generate new sources of “exports” from here to the increasingly energy- and climate-focused global marketplace (although this still will be highly competitive.)

Just as firms throughout the world will seek to manage their energy use and reduce their carbon output, so too will local firms look to hire or buy the best technologies or services in the marketplace. The challenge will be to make sure that our local cleantech firms are globally competitive enough to be able to sell their goods and services to the rest of the local economy. This will avoid what is called “economic leakage,” or the loss to outside markets of money that otherwise would be spent locally.

Beyond creating high-end technology and engineering jobs, the presence of a local cleantech industry has multiplier effects on the whole regional economy, creating jobs across a range of supporting industries, including both professional services that service the cleantech industry (law firms, architecture firms, investment firms and marketing firms) and green-collar jobs relating to the distribution, installation and maintenance of renewable-energy and energy-efficiency products.

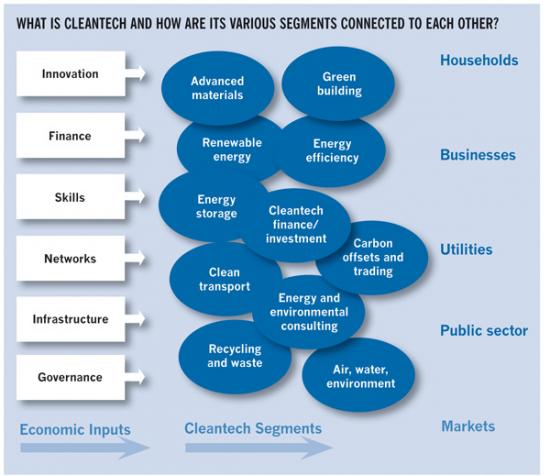

While cleantech is not a single unified industry, all firms in cleantech share an important characteristic: market demand from many buyers across businesses, households and governments who are all looking to manage their energy use or reduce their environmental impact. We argue that cleantech is made up of 11 different but overlapping industry segments. These segments all rely on inputs — like a skilled workforce or early-stage finance — to first design and develop, and then to bring their products or service to market.

The bottom line of the study’s conclusions, after compiling a database of 428 Bay Area firms working exclusively in cleantech and surveying cleantech experts and business leaders? San Francisco is doing well in such areas as green buildings, energy and environmental consulting, cleantech finance, and an emerging field of carbon offsets and trading. The city is also well positioned to make cleantech an even more important part of the local economy, providing a significant number of jobs at a variety of levels — if it seizes the opportunity to encourage cleantech businesses by building on its strengths and taking action to minimize its real and perceived weaknesses.

What is cleantech?

One of the challenges encountered in analyzing the importance of cleantech to the economy of San Francisco and the Bay Area is the question of what cleantech really is. While some observers and analysts might try to point to a discrete piece of technology and say that it is or isn’t cleantech, it probably makes more sense to take a broader view and to consider how those technologies are applied.

In that light, then, cleantech refers to a range of innovative products, processes and services that improve the efficiency of resource use and reduce environmental impacts. The common thread connecting these elements of cleantech is a shared ability to improve operational performance, productivity or efficiency while reducing the amount of materials used, energy consumed, or waste or pollution generated. The cleantech industry encompasses a broad range of products and services, from alternative energy generation to wastewater treatment, to more resource-efficient industrial processes. Many of these products and services may be useful to more than one kind of user, such as an insulating material that can improve the efficiency of a food refrigeration system and also serve as a heat shield in an industrial manufacturing process.

Some technologies, such as renewable energy generation, are inherently clean because their essential function is to provide a cleaner alternative to existing products. However, other technologies are not inherently clean, but an examination of how they are applied reveals that they produce a cleaner effect. For example, many nanotechnology firms are increasingly considered part of cleantech because their products can be used in a range of cleantech applications, from green building materials such as energy-efficient architectural glass and roofing applications, to lighter and stronger materials for building airplanes and vehicles that make them more fuel-efficient, to materials for producing thin-film solar cells. This highlights an important characteristic of cleantech: its pivotal role in the greening of the entire economy, as the products and services that emerge are integrated into many other industries.

In analyzing local cleantech industries, ICF took a broad view of cleantech and surveyed not only those businesses directly involved in researching or manufacturing new technologies, but also examined a range of related business activities that are critical to the growth of the cleantech industry, such as environmental consulting, solar-electricity installation companies, and cleantech finance and investment firms.

With this broad view of cleantech as a starting point, the ICF study first compiled a database of nearly 800 firms connected to cleantech in the Bay Area. A closer examination of all the firms revealed that there were only 428 firms that were entirely cleantech among the list. For example, many large firms such as General Electric have major divisions working in cleantech. However, the final database included only firms whose primary function was directly within cleantech. As a result, the results here are not inclusive of all firms working in cleantech or related industries (because that would encompass much of the entire economy).

Ultimately, cleantech is a grouping of industries and segments — organized into 11 general categories — which are connected by the theme of helping the rest of the economy respond to an increasingly environmentally-conscious and carbon-constrained world. It is a grouping that describes a phenomenon in the marketplace and a changing consciousness on the part of consumers, governments and businesses.

Even though cleantech is useful only as a temporary framework and concept, the segments that make up cleantech are categories that reflect growing industries, such as carbon trading, solar power, and advanced materials. The goal of identifying and describing cleantech is therefore to understand how competitive San Francisco and the Bay Area are in these key segments of cleantech. Economic development in a cleantech world will be in the cities and regions that are best able to develop successful firms across the many segments of cleantech and can export those services and goods to other places.

Cleantech’s place in San Francisco and the Bay Area

The Bay Area’s cleantech firms' market ranges from individual households to specific industries such as transport and construction, to major utilities and public agencies. Cleantech firms provide specialized products and services in many stages of the economy, from research and development to production and distribution, financing, distribution, installation, and service.

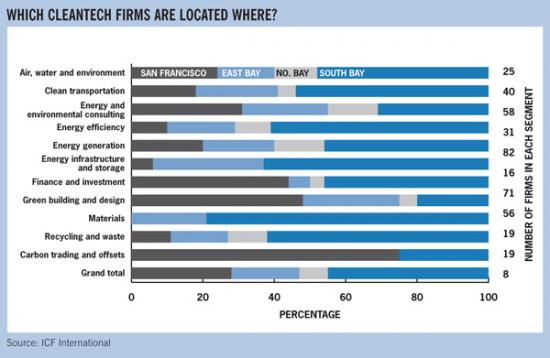

The majority of cleantech businesses in the Bay Area fall into six categories: renewable energy generation (the largest category, with three-quarters of these businesses focused on solar energy), finance and investment, energy and environmental consulting, green building and design, transportation, and energy efficiency.

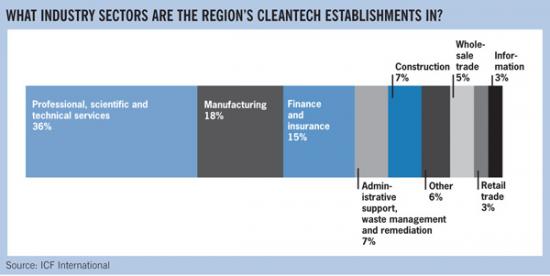

Across these six categories, Bay Area cleantech firms primarily fall into several major economic sectors. Over 40 percent are classified as professional, scientific or technical as well as administrative services. Over 18 percent are in manufacturing, 15 percent in finance and investment and the remainder in a mix of construction, wholesale trade, retail, and information. While cleantech is broad in the types of products, it is equally broad in the specific functions of the firms. For example, within the solar industry there are firms whose focus is designing and manufacturing a product, others who help finance solar projects, others who design software for solar, and still others who focus on selling and installing solar for the end consumer. This diversity of functions is as true in almost all of the cleantech segments as it is in traditional industries.

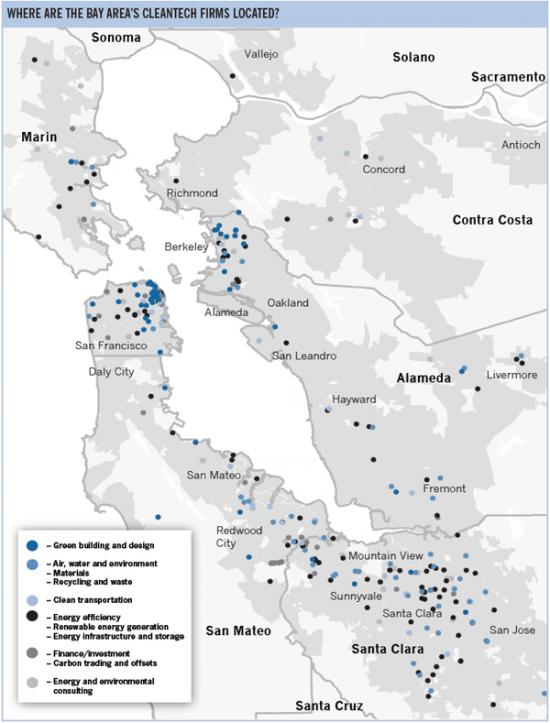

Most of the major sub-regions of the Bay Area have similar distributions of businesses in these categories, but San Francisco clearly displays a distinctive specialization in finance and investment, as well as in green building:

- San Francisco: Here cleantech establishments are most concentrated in finance/investment (26 percent), green building (23 percent), energy and environmental consulting (15 percent) and renewable energy generation (14 percent).

- South Bay: Here cleantech establishments are most concentrated in renewable energy generation (20 percent), finance/investment (17 percent), and clean transportation (11 percent).

- East Bay: Here cleantech establishments are most concentrated in renewable energy generation (21 percent), green building (19 percent), energy and environmental consulting (17 percent), and clean transportation (11 percent).

- North Bay: Here cleantech establishments are most concentrated in renewable energy generation (33 percent) and energy and environmental consulting (22 percent).

While many technology booms have been concentrated in Silicon Valley, cleantech is fairly evenly spread throughout the Bay Area. This is in part because cleantech firms serve such a broad range of markets and rely on such a broad range of workforce skills.

This study identified 428 cleantech establishments in the Bay Area of which 193 are in the South Bay, 118 in San Francisco, 81 in the East Bay and 36 in the North Bay. Certain segments are more concentrated in particular subregions, while cleantech firms in the East Bay and South Bay tend to be larger than in San Francisco.

The next section provides a deeper analysis of those segments that have the most promise for San Francisco. This is defined primarily as either San Francisco having a large share of the region’s firms in that segment or that segment making up a significant share of cleantech firms in San Francisco.

Overview of cleantech segments

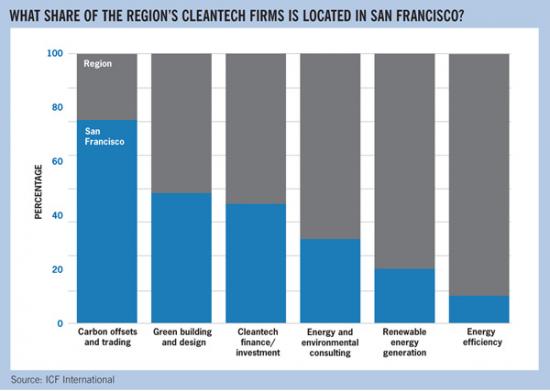

This category includes businesses providing project financing for renewable-energy and energy-efficiency projects, as well as venture capital, private equity and other investment firms that provide targeted funding for the development of cleantech ventures. This segment is critical to the overall growth of these industries, as early-stage financing is essential to the development of new technology and the creation of new firms, and innovative project-financing tools are increasingly important to make sure that end consumers are able to purchase and make use of the new technologies. The finance and investment segment of cleantech is the second-largest in the Bay Area cluster, representing 17 percent of all cleantech businesses in the Bay Area, with most of these being cleantech-focused venture-capital firms. This segment is even more important to San Francisco than to the broader region, as it accounts for more than one-quarter of San Francisco cleantech businesses.

Cleantech finance is a segment in which San Francisco, and the broader Bay Area, has a major competitive advantage. The region has been a center of high-tech financing since the 1980s and has leveraged this existing strength to become a leader in this new wave of investing. One of the world’s first dedicated clean energy venture-capital firms, Nth Power, is based in San Francisco, and many Silicon Valley venture-capital firms such as Kleiner Perkins Caufield & Byers and Draper Fisher Jurvetson have launched cleantech or greentech funds. Bank of America has committed $20 billion to support environmentally-sustainable business. San Francisco should continue to explore creative ways to bring together the region’s financial expertise and resources to accelerate the growth of its cleantech industries.

This is another area in which San Francisco enjoys a significant advantage with over 45 percent of the region’s green building and design firms located in the city. This portion of cleantech includes architectural, design and construction firms that focus on the development of energy-efficient and environmentally sustainable buildings, as well as firms involved in the production of reduced-waste and high-performance building materials. This segment makes up 13 percent of the overall Bay Area cleantech cluster, with green architecture and design constituting 61 percent of establishments in the segment and green building materials constituting 23 percent.

Promoting green building in San Francisco is important for meeting the City’s environmental and economic objectives. Since approximately half of all emissions in San Francisco come from buildings and other stationary sources, improving the efficiency of buildings can go a long way toward meeting the City’s climate objectives. And the green building industry is an important economic-development opportunity, due to the high number of quality jobs in design, engineering, construction, and building maintenance it can create.

San Francisco could continue to leverage its strong architecture, design and construction industries to become a leading center for green building. One particular opportunity is for the city to explore ways to combine its strengths in green building, energy efficiency consulting, and finance to conduct building retrofits on a large scale in specific types of structures. There is a great demand for retrofitting buildings to achieve greater energy efficiency, and many cities are seeking ways to do this block by block instead of building by building. Competition for this market segment will be substantial, but the demand will be very large given that there are several hundred thousand buildings in the city.

This segment of cleantech includes firms involved in the research and development, manufacturing, design, installation, maintenance, and management of systems for generating energy from solar, wind, geothermal and other renewable sources. While this segment accounts for 20 percent of all cleantech establishments across the Bay Area, it is less concentrated in San Francisco, accounting for

only 14 percent of local businesses. However, two renewable energy sub-segments represent potential opportunity for San Francisco: solar, wind and tidal energy.

San Francisco’s best opportunity in solar energy generation doesn’t lie in something such as manufacturing the materials for solar panels, however. Activities such as system design, installation and servicing are the most viable solar opportunities for San Francisco, as they require site management and client interaction and need to be locally based. In terms of manufacturing, areas of opportunity could be the later stages of photovoltaic system assembly such as production of solar modules or panels. Module assembly involves packaging and electrically connecting a number of solar cells, while panel assembly involves mechanically fastening and wiring a collection of these modules together, and often encasing them in a frame and glass covering. This is the first point in the process from raw materials to consumers where it is beneficial for the producer to be located close to consumer demand, which makes this later-stage assembly a potentially viable activity in a market with higher real-estate costs such as San Francisco.

While large-scale wind-power facilities may not be suitable for most parts of the Bay Area, small wind-power projects creating less than 100 kilowatts hold more promise. San Francisco is starting to focus on this niche segment, and the mayor recently issued an executive order to City departments to speed up the granting of permits for small wind projects. Newsom and members of the Board of Supervisors also have gathered a 20-member task force (which SPUR is a member of) and 12 technical advisers to figure out how best to encourage the development of more urban wind-power projects. The task force may explore issues such as changes to zoning to encourage wind projects and the development of an incentive program.

While San Francisco has 28 percent of the 428 cleantech establishments in the Bay Area, it has a significantly higher percentage of the region?s cleantech establishments in three segments: carbon trading and offsets, green building, and finance.

This is another promising area for San Francisco. At a time when California is moving toward mandatory carbon caps and national climate legislation is expected, many large U.S. corporations, including PG&E, are now supporting cap-and-trade legislation. The Bay Area has a number of young firms that specialize in selling renewable energy credits and emissions offsets and in advising firms on offset strategy and purchases. San Francisco has the majority of firms in this small but growing segment which cuts across many functions — from identifying offset projects internationally to financing offsets or trading emissions to developing software for tracking investments to auditing compliance. While not included as firms in this study, there is significant growth in carbon trading and offsets within traditional financial institutions. Increasingly, a number of large banks, financial institutions, and nonprofit organizations are establishing new practices focused on emissions trading. San Francisco should continue to cultivate its leading position in this specialized industry, leveraging its strengths in finance, environmental policy and consulting.

Finally, professional services are also a promising segment in cleantech. While not analyzed as a distinct segment within cleantech, professional services are important due to an ongoing trend in which existing professional services firms — particularly law, management consulting and public relations — are retooling themselves to target and serve emerging cleantech markets as a distinct market segment. Many firms are establishing cleantech-focused departments or practices, and others are reinventing themselves to focus exclusively on cleantech. These firms play an important role in both supporting the development of the cleantech industry and in speeding the adoption of these technologies by consumers and businesses. As these firms develop specialized knowledge and a track record of success working on cleantech issues, these services increasingly can become an important export for San Francisco’s companies.

San Francisco’s homefield advantage

Successful new industries form and mature in regions that have both the demand for certain products or services, and the materials or knowledge needed to supply that demand. The Bay Area and San Francisco possess these kinds of advantages in a number of areas, placing the region in a good position to become a leader in cleantech. Specifically, San Francisco has strength as a center for innovation, finance, a skilled workforce and physical infrastructure. It also gains positive marks for aspects of its governance, but there is room for improvement.

Countries and regions have long admired and emulated the characteristics of the Bay Area, and Silicon Valley in particular, with its distinctive economic dynamism: a high rate of enterprise formation in leading fields of innovation, a continued stream of these firms that mature into a viable industry and an ability to capture the highest portions of the value-chain over time. This historic advantage is not even in all fields or industries, yet for those that grow — and there are many — there is clearly a natural “vital cycle” in which the inputs that are available — whether innovation from universities or other firms; capital from high net-worth investors or venture funds; skilled workforce that is mobile; infrastructure that enables logistical efficiency; appropriate government regulation and support of enterprise formation, growth and attraction — subsequently draw in more innovation, workforce skills, industry investment and supporting supply-chain (even in an era of outsourcing).

Every region has an “innovation pipeline.” This pipeline is the aggregate of public and private research, study and discovery; the development of discoveries and innovations into new technologies and products; and the deployment of these products into the marketplace.

The discovery portion of San Francisco’s innovation pipeline consists of research universities, institutes and laboratories. These institutions are centers of research, and generate scientific publications and intellectual property. They also train students and workers. The development system is made up of companies that harvest discoveries from their own research as well as research by outside sources, from which they develop technology and products in their own laboratories. The development portion also includes startups — companies that are newly founded upon the potential of one or more discoveries. The deployment system consists of companies and their marketing, sales and distribution partners.

Innovation is the key requirement for the growth of many cleantech firms. Over one third of firms surveyed for this study indicated that proximity to innovation centers was extremely important to their location decisions. Over 40 percent stated that it was somewhat important.

The Bay Area innovation pipeline is strong, and the historic relationship between local industries and the University of California system, Stanford, the national laboratories, and California State University campuses has been a major advantage for virtually every technologically driven industry in the region, including cleantech. The agglomeration of technology enterprises around the University of California and Stanford reflects the importance of these institutions as important feeders of the innovation pipeline. Historically, much of the Bay Area’s research has focused on information technology, semiconductors and bioscience. However, both Stanford and UC Berkeley recently have established cleantech and energy-efficiency research institutes with annual budgets of more than $100 million, and grant-funded research in the clean-energy and energy-efficiency fields exceeds $300 million annually at both institutions.

Within each cleantech segment, firms are serving many distinct functions and even different end markets. For example, some solar companies may be working on product design and manufacturing, some on developing software to measure the energy output of a solar system and others on selling and installing solar systems on homes.

Despite the lack of a research university in San Francisco focused on cleantech, the city rated strongly among surveyed firms. 80 percent of respondents to ICF’s cleantech survey felt that San Francisco rated favorably or very favorably with respect to its proximity to innovation centers. Firm-specific interviews further supported the perception that San Francisco was well positioned to take advantage of research and discoveries in the region. Still, several respondents felt that more could be done to strengthen its ties with these institutions and leverage their capabilities through activities, such as establishing commercialization programs to help launch San Francisco-based spinouts, recruiting staff and interns in San Francisco cleantech companies, and sponsoring seminars and technology conferences.

One of the major constraints for San Francisco, however, is the cost of commercial space and the limited availability of space for manufacturing. To address this limitation, San Francisco could develop a location for cleantech industrial growth both to change the market perception about opportunities for location in San Francisco, and to provide a visible hub for cleantech activity, much as the City has done for life sciences through the development of Mission Bay.

The Bay Area is strong in another essential building block of a successful cleantech economy: finance. The region is known for its deep and broad capital market that focuses on developing technology-based enterprise, and investors have thoroughly embraced the cleantech industry. Cleantech is now a mainstream financial investment market in the Bay Area, and around much of the world.

With more than 40 percent of venture investment in clean energy occurring in the Bay Area, venture financing does not seem to be the limiting factor to the growth of cleantech in the region. The key gap in the financial pipeline in the Bay Area, and particularly in San Francisco, is early-stage seed financing. Notably, as venture funds have grown in size due to the influx of institutional investment over the years, the funds’ interest in early-stage investment placements has declined. Today, a very small portion of total venture fund placement is in early-stage enterprises. More of the capital is now invested in firms that are more mature. This creates an abiding challenge for growth of innovation-driven firms at the earlier stages—including cleantech.

In surveying cleantech businesses about their location decisions, access to a skilled workforce was cited as the most important factor: Ninety-two percent of firms indicated that access to skilled labor was somewhat or extremely important, with more than 60 percent saying that it was extremely important.

In terms of high-skill workforce, the Bay Area has a much higher concentration of knowledge-based professionals and executives than the rest of the nation, and 35 percent of adult residents hold a bachelor’s degree or higher. San Francisco has an even higher average, with nearly 50 percent of workers living in San Francisco holding a bachelor’s degree. San Francisco has a dynamic business community with many of the type of business leaders — chief executive officers, chief financial officers and mid-level managers — needed to grow cleantech companies. Even stronger is the diverse group of professional firms — lawyers, marketing and public-relations firms, bankers, accountants, and architects — that provide key services to these firms as they are being established and maturing.

Research for the ICF report found that 80 percent of those surveyed perceived San Francisco’s skilled workforce to be an advantage.

The presence of corporate headquarters for both the California Public Utilities Commission (CPUC) and the state’s largest regulated utility (PG&E) in San Francisco is seen to further enhance the city’s reputation as a leading destination for professionals seeking careers in energy efficiency, renewable energy, and other areas of cleantech.

One area of workforce skills where San Francisco is comparatively weaker is engineering. No engineers interviewed for this report perceived San Francisco as a compelling location for cleantech work. The sentiment was that cleantech engineering was the domain of Silicon Valley. Changing this perception will be important to attracting and retaining the technical workforce needed to support the development of cleantech in San Francisco.

San Francisco also faces the challenge of creating cleantech job opportunities for its less-educated citizens and building a workforce-development system that enables more of the city’s residents to reap the economic benefits associated with the growth of these industries. The planned cleantech development at Hunters Point, which will employ green building techniques throughout much of the planned construction, provides an excellent opportunity for expansion of efforts to get more residents into green-collar jobs.

Just as San Francisco’s existing workforce brings both advantages and difficulties, the physical infrastructure available to cleantech businesses is suitable to some and challenging for others. Not surprisingly, San Francisco’s cleantech cluster is most heavily concentrated in segments that are suited to being located in commercial offices, as opposed to those that require more industrial facilities.

The majority of negative comments about San Francisco encountered when surveying cleantech businesses related to the cost of commercial space and transportation infrastructure. Ninety-two percent of respondents felt that the cost of commercial space was either extremely or somewhat important to their location decisions, and 75 percent felt that San Francisco rated unfavorably on this factor.

Access to parking was slightly less of a concern than expected. Less than half felt that availability of parking was an important factor in their location decisions. By contrast, proximity to public transport was either extremely important or somewhat important to 72 percent of survey respondents, and 74 percent felt that San Francisco’s access to transit rated favorably. These results are important as they highlight how the attitudes of cleantech companies towards parking and transit may differ from other technology-based startups such as biotech.

The ICF survey also asked cleantech firms to state the types of facilities they would seek if they were to move or open new operations. While 44 percent said they would seek a downtown office, 46 percent said that they would need flexible, lower-cost office space outside of downtown San Francisco, and 29 percent would seek manufacturing or industrial space.

As San Francisco evolves its strategy to develop cleantech, planners and economic development officials should be aware of the needs of companies in particular technology segments and at different stages of their development. Many startups need flexible space with short-term and flexible lease structures. Solar firms will need industrial space to carry out light manufacturing related to assembly of modules and system, as well as sunlit open space for demo and testing.

The City should continue to pursue its plans for developing the Hunters Point Shipyard and nearby India Basin as a site for the agglomeration of cleantech-related businesses. As it does so, the City should attempt to ensure that there is sufficient transit infrastructure in place to service this location, and that the zoning is flexible enough to enable the cleantech firms to remain in the city as they advance from their startup phase into production and beyond that into sales and potentially broader corporate management functions.

Governance: Simplifying rules and procedures

The final major building block of an environment conducive to the growth of cleantech industries is governance. A city’s public policies and administrative procedures can stimulate or inhibit the growth of an industry. Policies that are viewed as constraining or inhibiting the formation, expansion and attraction of enterprises include inefficient permit processes, unclear or inappropriate taxes, and inconsistent or burdensome regulations. San Francisco has already taken a step to reduce its payroll tax for cleantech firms. However, given the challenges of appropriately defining cleantech (which could be claimed by large parts of the economy), the participation in the tax incentive is minimal and not yet an important tool for significant business attraction. At the same time, cities can enact policies that play a critical role in fostering enterprise growth by creating demand for cleantech products and services, thereby supporting the growth of local firms and good quality green jobs. In the broadest terms, local government can stimulate this demand in two ways: through direct public-sector investments or through public policy that establishes incentives, standards, and mandates. Investments include actions such as retrofits or new construction on public buildings to make them more energy efficient implementing demand-response programs and commitments to purchase cleantech products such as alternative vehicles. Standards, incentives and mandates include green building requirements, local clean energy incentives, or industrial land preservation with flexible zoning that supports the hybrid nature of many cleantech businesses (i.e. a mix of office and production).

In the ICF cleantech survey, the development of consistent City policies to stimulate demand for cleantech products and services was given the highest ranking of all proposed interventions, with 82 percent of firms saying that development of consistent City policies designed to stimulate cleantech industry growth was either very important or critical. More than half of all respondents rated this as critically important.

The mayor and the Board of Supervisors have played an active role in developing environmental policy initiatives, including efforts to promote a green fleet of City vehicles, promoting the construction of energy-efficient buildings and climate action goals to reduce the city’s overall emissions. While important, most of these policies are focused on environmental, not economic development goals. As a result, there is little direct connection between the policy and the growth in firms and employment in cleantech (beyond the important aspects of San Francisco being perceived as a center for innovation in environmental policy). Recently, the City passed the nation’s highest local solar subsidy, providing up to $6,000 in rebates to households and up to $10,000 to businesses that install photovoltaic systems. Because this solar program included the highest incentive for hiring a firm with a graduate of a local workforce program, it is expected to lead to more solar firms relocating to the city and the creation of hundreds of green-collar jobs.

Despite the current enthusiasm for solar installation, there is a risk that this one segment of the industry may become overemphasized. Competitive market forces, the continuation of state and federal tax credits and the limited size of the local market will ultimately determine the number of solar installation companies and jobs that survive in San Francisco. A long-term economic development perspective should also focus on supporting the firms who export their products beyond the city.

Further, these concerns should also be taken into account when designing green jobs programs, as there is a risk of oversaturating the market with trained solar installers. There are many other promising job segments in cleantech (such as energy retrofits) which could also be candidates for incentives.

Moving forward, the City should continue to develop green policies that systematically integrate environmental objectives with economic development goals.

Cultivating San Francisco’s cleantech economy

The evolution of cleantech is a very significant economic opportunity for San Francisco and the Bay Area as a whole. As companies and regions throughout the world seek to reduce their environmental impact, they will look to the firms that offer the most innovative and advanced solutions. As has happened for most prior technology-based booms, these firms may likely be clustered in several regions throughout North America and the world. San Francisco has a chance to play a leading role in the Bay Area, which is already one of the global centers in cleantech.

Considering the relative advantages and challenges confronting San Francisco as it seeks to grow its cleantech businesses and jobs, what is the best path? In brief, the City and private sector together should throw much of their weight into emphasizing and developing the strengths San Francisco already possesses instead of chasing after the types of cleantech businesses and jobs that need things the city will find difficult to provide.

Broadly speaking, San Francisco should seek to build on its leading position in green building, finance, carbon offsets and professional services, as opposed to trying to establish strength in other areas such as materials, energy infrastructure, and clean transportation. In order for cleantech segments to develop and mature, they must be able to draw on key economic inputs or “foundations” — innovation, skills, finance, infrastructure and governance — provided by the region in which they are based. The City and private sectors must work jointly to continually improve and strengthen these foundations to provide local firms with the advantages they need to innovate and grow.

San Francisco’s strongest inputs include access to skills, finance and innovation while its governance system includes both strengths and weaknesses. Key to the governance system’s strengths is the far-reaching environmental policies that set new standards on the marketplace as well as bring attention to the city as a leader. Yet many of these policies are disconnected from economic development goals and thus have minimal relationship to growing cleantech firms. As a comparison, the city of San Jose has a green vision that combines a goal of creating 25,000 cleantech jobs with ambitious environmental goals such as reducing per capita energy use by 50 percent and retrofitting 50 million square feet of buildings.

A key question facing public and private leaders as they consider how best to help grow cleantech in San Francisco is whether cleantech should be treated as a distinct industry or should be viewed as a series of distinct segments which are increasingly a natural part of existing industries. This question is important for one particular reason: if cleantech is treated as a single industry — though broad and evolving —success will be measured by growth of firms, employment, and investment in cleantech in the aggregate. If its segments are treated as a series of separate industries, policy intervention will vary by segment.

This article has argued that cleantech is not a distinct industry, in much the same way that “high-tech” is not an industry. Instead, cleantech is reflective of a series of enabling technologies which are increasingly important inputs across all existing industries. Still, cleantech is useful today as its own category that emphasizes improved energy and environmental performance. As such, cultivating cleantech in San Francisco requires maintaining a common focus on baseline conditions that will enhance broader enterprise formation, expansion and attraction.

A cleantech strategy for San Francisco should build in the following three principles:

The principle here is that economic development efforts focusing on cleantech should build on the existing segments that have established themselves in the city, not segments (such as recycling or waste) that may be desirable but have minimal local presence. The goal should be to leverage current concentrations and to assist these segments to deepen and broaden their value-chains, with the anticipated outcome of creating new jobs and economic value.

The principle here is to identify and provide distinctive inputs needed by cleantech firms to enable their growth. This means that in order to form new enterprises, to expand existing ones and to attract new firms, San Francisco must work to continually improve the responsiveness of its economic input foundations to cleantech—in workforce, innovation, finance, infrastructure, and governance. Improving these inputs are not the exclusive responsibility of the City and County, as strength in skills, finance and innovation are more based on private action than public policy.

Successful markets are intrinsically about collaboration—recognizing value and making transactions. In order to implement a vision for cleantech development, San Francisco needs to foster collaboration among cleantech firms and between the public and private sector users or buyers, to more effectively share information, align public inputs to needs of local businesses, and develop partnerships on key opportunities. Leadership in cleantech will require both public sector vision and private sector action.

Based on these general ideas, we propose a number of potential strategic directions and actions for enhancing and accelerating the development of cleantech in San Francisco:

- Bring together the public and private sectors (including local utilities) across key cleantech segments to collaborate on a series of strategies for growing cleantech firms and integrating cleantech solutions into the overall economy. The city has already begun such an approach through its solar and wind power task forces. That model should be expanded to include participation of a broader cross-section of stakeholders – finance, education, other suppliers and customers.

- Develop a cleantech research/eco-industrial park at a location such as Hunters Point or Pier 70, where cleantech companies can work together to develop and implement new solutions on site. Such a park could be connected to an incubator for new businesses and would focus on specific segments such as renewable energy, green buildings and energy efficiency.

- Form partnerships with key educational and research institutions in the Bay Area to strengthen the innovation pipeline.

- Create a seed fund to provide early-stage capital to local cleantech companies so they can pursue promising ideas.

- Establish a green jobs program to broaden the economic benefits of cleantech development across a number of income levels. Ensure an adequate focus on current promising areas such as energy efficiency and building retrofits.

- Support demonstration centers of cleantech products (such as the PG&E Energy Center) to test their effectiveness and speed their integration into the marketplace.

- Pursue cleantech events and conferences to ensure that San Francisco maintains its presence as the center for thought leadership and networking in cleantech. While San Francisco is already among the leading locations for such events, the recent relocation of the marquee West Coast Green to San Jose highlights the importance of focusing on this current strength, particularly because green building and design is one of the few industries where San Francisco currently outshines the South Bay.

- Develop specific implementation targets for a cleantech vision to help market San Francisco to the outside world as well as to drive demand for and adoption of cleantech products and services locally. Such targets should be defensible based on realistic assumptions for both firm creation and the integration of cleantech.

These brief recommendations represent an outline for a course of action, given what we know about cleantech as it exists today. Even if specific segments of cleantech experience significant changes, however, San Francisco can put itself in a good position to adapt by following the general principles of building upon what it already knows how to do, maintaining and enhancing the building blocks of good business conditions here, and forming well-chosen partnerships with both producers and consumers as well as the institutions that generate innovations.

The ultimate goal is for San Francisco to be both a center of cleantech innovation and firm creation as well as to ensure that the rest of the economy adjusts to the growing reality of climate change and the need for effective environmental and energy management. By recognizing the role of cleantech in that transition, we will not only develop a more competitive economy, but also reduce our overall environmental impact.