As the deadline rapidly approaches to submit measures for the November ballot, the City and County of San Francisco is moving ahead aggressively with its effort to reform the city’s business tax. While the city has made significant progress in recent weeks, there are some signs that the complexity and commitment to reform are being further complicated by increasing calls for a tax that would not just replace revenue from the existing payroll tax but bring the city additional funds.

City Controller Ben Rosenfield and Chief Economist Ted Egan have for the last few months been hard at work designing a replacement for San Francisco’s payroll tax. The controller’s office originally modeled two different proposals to replace the city’s current payroll tax: a modified payroll tax that would lower rates and broaden the base of payers, and a gross receipts tax based on rate schedules defined by industry. In the last month, however, that process has narrowed to focus solely on a gross receipts tax proposal. (Read the controller’s latest report on that effort.)

Gross receipts taxes are widespread in California, but they all have one important thing in common: They are extremely complicated. The tax must address dozens of different industries, as well as companies’ differing abilities to pay — and their varying ability to move to other places to conduct business. All this means there are many more levers than with a simple payroll tax. (San Francisco’s existing payroll tax is a straight 1.5 percent of all payrolls over $250,000 per year.)

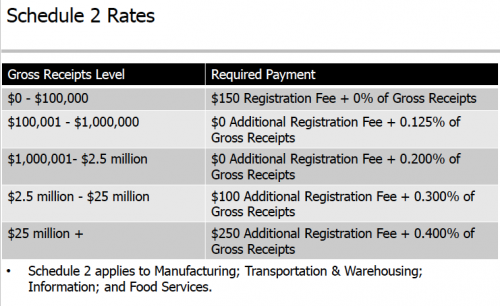

But with a multitude of levers also comes significantly more flexibility. For example, the controller’s current proposed structure consists of six separate schedules. These schedules group companies that have comparable ratios between payroll (an expense) and gross receipts (how much money a company makes). For example, a real estate management firm may have few employees and high gross receipts from rent and other fees paid by tenants. Conversely, a restaurant might have a large number of employees and lower overall receipts. These two very different operating models are treated identically under the city’s existing payroll tax, but a gross receipts tax would provide different schedules for types of companies with different cost structures.

Another goal of the controller’s effort is to attempt to make the tax structure progressive in order to encourage job growth in small businesses and start-ups. Within these schedules there are a number of different rates (see sample schedule below) so that companies generating more revenue within each category would pay marginally higher rates. Likewise, start-up businesses that are not yet generating revenue — but may have significant payroll as they build products or services — would have more breathing room than they do in the current structure.

![]()

Source: San Francisco Controller’s Office, “San Francisco Business Tax Reform: Status Report on Work to Date,” May 10, 2012.

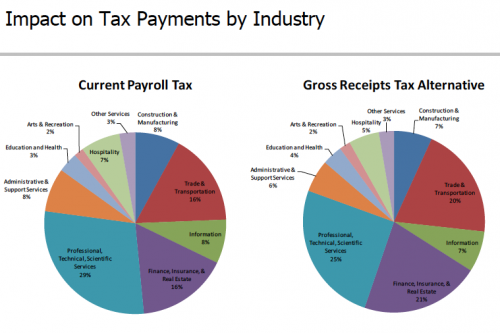

While the process to date has been one of the most inclusive in memory — with dozens of industry meetings and numerous iterations — the devil will ultimately be in the details for any proposal submitted to voters. There will be many winners and losers in any transition to a new tax (see below), which means achieving some form of consensus could determine a measure’s success or failure.

The eventual success or failure of business tax reform in San Francisco is only partially dependent on the structure of the proposal itself. The other side of this coin has to do with revenue. By design, all proposals to date have taken a “revenue neutral” approach; they attempt to simply replace revenue from the payroll tax and not generate additional funds for the city. However, that original intent is increasingly in doubt as the June deadlines for the ballot approach. Supervisor John Avalos, officials from Service Employees International Union 1021 and others have indicated their desire for any changes to the tax to generate additional funds. Whether or not those hopes are eventually included in the mayor’s tax reform proposal, it is increasingly likely that a separate measure to increase revenues could also be on the ballot in November. Could the controller’s measure include some additional revenue in order to neutralize these efforts?

The final stretch of negotiations will be critical to the success of the city’s business tax reform efforts. With the multitude of different moving pieces — both within the negotiations over rates and financial impacts, and apart from the negotiations around new revenues — this is still a fragile coalition. We hope a balance can be struck that will allow for the city to successfully transition to the gross receipts tax currently on the table. It would allow for greater stability over time, more equity and built-in incentives for new companies and industries to grow and thrive in San Francisco. But we must be mindful of the delicate balancing act required to get there.